Bahrain ESG Reporting: What CBB-Licensed Banks Must Know in 2026

Bahrain ESG Reporting: What CBB-Licensed Banks Must Know in 2026

Bahrain has moved ESG reporting from aspiration to obligation. The Central Bank of Bahrain (CBB) issued its Environmental, Social and Governance (ESG) requirements module in November 2023, making sustainability disclosure mandatory for all CBB-licensed banks, financing companies, insurance firms, and investment firms from financial year 2024 onwards.

If your institution is CBB-licensed and you have not yet built a structured ESG reporting programme, you are already behind. This article covers the framework requirements, the Islamic finance dimension, how Bahrain compares to Qatar and the UAE, and what your compliance team must do now.

Source: Central Bank of Bahrain, ESG Requirements Module, November 2023

What Are the Mandatory ESG Reporting Requirements for Companies in Bahrain?

The Central Bank of Bahrain (CBB) issued its ESG Requirements Module in November 2023, making sustainability disclosure mandatory for financial year 2024 onwards. The module applies to all listed companies, banks, financing companies, insurance firms, and category 1 and 2 investment firms licensed by the CBB. There is no phased-in grace period and no minimum size threshold for banks. If your institution is CBB-licensed, you are in scope.

Source: Central Bank of Bahrain, ESG Requirements Module, November 2023

The module draws on GRI (Global Reporting Initiative) Standards as its primary framework and incorporates TCFD guidance for climate-specific disclosures. Unlike the ISSB model adopted by Qatar, Bahrain uses double materiality: entities must disclose both how ESG factors affect the business financially, and how the business itself affects the environment and society. The full set of required KPIs is listed in Appendix 1 of the CBB module.

Source: Green Central Banking, "Central Bank of Bahrain Issues ESG Requirements," November 2023

The table below maps the specific obligations under the CBB framework.

What Happens If You Miss the Deadline?

The CBB has enforcement powers under Articles 38 and 65(b) of the Central Bank of Bahrain and Financial Institutions Law 2006. Non-compliance with the ESG module exposes CBB-licensed entities to regulatory intervention, including formal notices, restrictions on licensing activities, and reputational consequences with institutional investors. There is no explicit published penalty schedule in the ESG module itself, but given the CBB's track record on governance enforcement, the risk of inaction is not theoretical.

Source: CBB Rulebook ESG-1; CBB and Financial Institutions Law 2006, Articles 38 and 65(b)

Bahrain Islamic Bank's 2024 sustainability report was independently audited by KPMG Fakhro and approved at board level, which signals that third-party assurance is quickly becoming market expectation rather than regulatory minimum. Banks that cannot produce audit-ready ESG disclosures are already at a competitive disadvantage in institutional financing and sukuk issuance.

Source: Bahrain Islamic Bank 2024 Annual Financial and Sustainability Report

Bahrain Bourse ESG Obligations for Listed Companies

Listed entities face an additional layer of disclosure. Bahrain Bourse updated its Listing Rules in November 2024 to incorporate the CBB ESG module into its formal listing requirements. The Bourse also publishes its own ESG Reporting Guide covering 32 specific ESG metrics. Any bank listed on Bahrain Bourse must align to both the CBB module and the Bourse guide simultaneously. The CBB's Common Volume ESG Module applied to all listed companies for the reporting period ending December 2024, with the updated Listing Rules effective immediately.

Source: Bahrain Bourse, Updated Listing Rules and Guidelines, November 2024

For a practical guide to what your compliance team should produce first, see the five steps for CBB-licensed banks detailed earlier in this article. If your institution also operates in Qatar or the UAE, Spectreco's guide to GCC ESG compliance requirements across all three markets covers the differences and overlaps in a single reference.

What the CBB ESG Module Actually Requires

The CBB framework applies to all listed companies, banks, financing companies, insurance firms, and category 1 and 2 investment firms. Reporting started for financial year 2024. There is no phased-in grace period for CBB-licensed banks.

The Core Framework Structure

The CBB module draws primarily on the Global Reporting Initiative (GRI) Standards and incorporates Task Force on Climate-related Financial Disclosures (TCFD) guidance. The TCFD is a global framework, established by the Financial Stability Board, covering four core disclosure pillars: governance, strategy, risk management, and metrics and targets.

The module includes double materiality: entities must disclose both how ESG issues affect the business financially, and how the business affects the environment and society. This places the CBB framework closer to the European model than to the purely investor-focused ISSB approach used in Qatar.

Scope of emissions required under the CBB module:

- Scope 1: Direct greenhouse gas (GHG) emissions from sources owned or controlled by the entity.

- Scope 2: Indirect emissions from purchased electricity, heat, steam, or cooling.

- Scope 3: All other indirect value chain emissions, including financed emissions (Scope 3 Category 15) for banks and financial institutions. Financed emissions represent the GHG footprint embedded in a bank's loan book and investment portfolio. For most banks, financed emissions account for over 95% of their total carbon footprint.

Annual Reporting Obligation

Listed companies and CBB licensees must submit an ESG report annually. The report must incorporate the ESG Key Performance Indicators (KPIs) specified in Appendix 1 of the module. It can either be a standalone document or included within the annual report.

The Bahrain Bourse also publishes its own ESG Reporting Guide covering 32 ESG metrics. Banks operating as listed entities on Bahrain Bourse must align to both the CBB module and the Bourse guide simultaneously.

Source: CBB Rulebook ESG-1, Thomson Reuters/CBB Rulebook Portal; Bahrain Bourse ESG Reporting Guide

Is Bahrain Adopting ISSB IFRS S1 and S2?

IFRS S1 and IFRS S2 are the two International Sustainability Reporting Standards issued by the International Sustainability Standards Board (ISSB) in June 2023. IFRS S1 covers general sustainability-related financial disclosures; IFRS S2 covers climate-related disclosures specifically.

Bahrain has not yet mandated IFRS S1 and S2. The CBB currently requires banks to report in line with TCFD and ISSB guidance, but broader ISSB adoption remains voluntary as of mid-2026. The CBB module treats TCFD as a reference framework, not a standalone requirement. Banks choosing to align early with ISSB S1 and S2 are working ahead of the curve, and the direction of GCC regulatory travel makes that a defensible investment.

The comparison across the GCC:

Qatar's approach is more prescriptive: the Qatar Central Bank (QCB) and the Qatar Financial Centre Regulatory Authority (QFCRA) have both mandated full IFRS S1 and S2 for financial institutions from January 2026. Bahrain is at an earlier stage but is expected to converge toward ISSB as GCC frameworks harmonise. Banks that build ISSB-aligned data infrastructure now position themselves to absorb that transition at lower cost.

The Islamic Finance ESG Angle: Why Bahrain Is Central

Bahrain is one of the world's leading Islamic finance centres. According to the Islamic Finance Development Indicator (IFDI) Report 2025, Bahrain ranked eighth globally in Islamic finance, with the Cambridge Institute of Islamic Finance placing it fifth in 2024.

Source: The Business Year, "Bahrain's Role in Islamic Banking and Finance," March 2026

Islamic finance and ESG share structural principles: both exclude harmful activities, both emphasise social responsibility, and both require transparency on the use of capital. This alignment creates a commercial opportunity for Bahrain's CBB-licensed banks.

Green Sukuk and the ESG Reporting Connection

Green sukuk are Shariah-compliant fixed-income instruments where proceeds are restricted to climate-positive or environmentally beneficial projects. ESG sukuk global issuance has grown sharply in recent years. In 2020, issuers sold $4.8 billion of ESG sukuk. By 2024, that figure had risen to $15.2 billion according to LSEG data.

For Bahrain banks considering green sukuk issuance, credible ESG reporting is not optional. Investors and underwriters require verified ESG data. Bahrain's Infracorp, part of GFH, issued a $900 million green sukuk. That issuance depended on a credible ESG framework to attract investor capital. Robust ESG reporting, aligned with the CBB module, is the foundation that makes such capital market access possible. Our Green Sukuk & ESG Disclosure in the GCC guide covers the issuance requirements in detail.

Source: Gulf News, "Bahrain's First-Ever Green Sukuk," Infracorp / GFH

The broader GCC sustainable finance market reinforces this pressure. S&P Global projects Middle East sustainable bond issuance to reach $20-25 billion in 2026, up from a 3% increase in 2025 against a 21% global decline. Sustainable sukuk volume in the Middle East reached a record $11.4 billion in 2025. Bahrain's banks that cannot demonstrate credible ESG data will find institutional capital increasingly difficult to access.

Source: S&P Global / Arab News, "Middle East Sustainable Bond Issuance to Hit $25bn in 2026," February 2026

How CBB Requirements Compare to UAE and Qatar

The three frameworks differ in depth, reference standards, and enforcement context.

The UAE Climate Law (Federal Decree-Law No. 11/2024) mandates GHG reporting through the Ministry of Climate Change and Environment's (MOCCAE) own MRV methodology. It is primarily a Scope 1 and Scope 2 emissions reporting obligation, enforced via the mrv.ae platform. The first reporting deadline was 30 May 2026. It does not produce a full ISSB-compliant sustainability report on its own.

Qatar's QCB and QFCRA have adopted IFRS S1 and S2 as mandatory for banks and regulated financial institutions from January 2026. Qatar uses a dual-regulator model: the QCB governs onshore banks, while the QFCRA governs QFC-authorised firms under the GENE Rules 2025. A bank operating in both jurisdictions must comply with both simultaneously. Spectreco's detailed breakdown of the UAE Climate Law and GCC ESG requirements covers this in full.

Source: Spectreco, "UAE ESG Compliance: What the 30 May 2026 Deadline Means for GCC Businesses," May 2026

Bahrain's CBB module sits between the two. It is more comprehensive than UAE's climate-focused MRV requirement because it covers full environmental, social, and governance disclosure. It is less prescriptive than Qatar's mandatory IFRS S1/S2 mandate because it draws on GRI and TCFD as frameworks without yet mandating full ISSB adoption.

For a financial institution operating across all three markets, a unified ESG data platform is the only practical solution. Building separate data silos per jurisdiction is a compliance and cost problem that compounds annually.

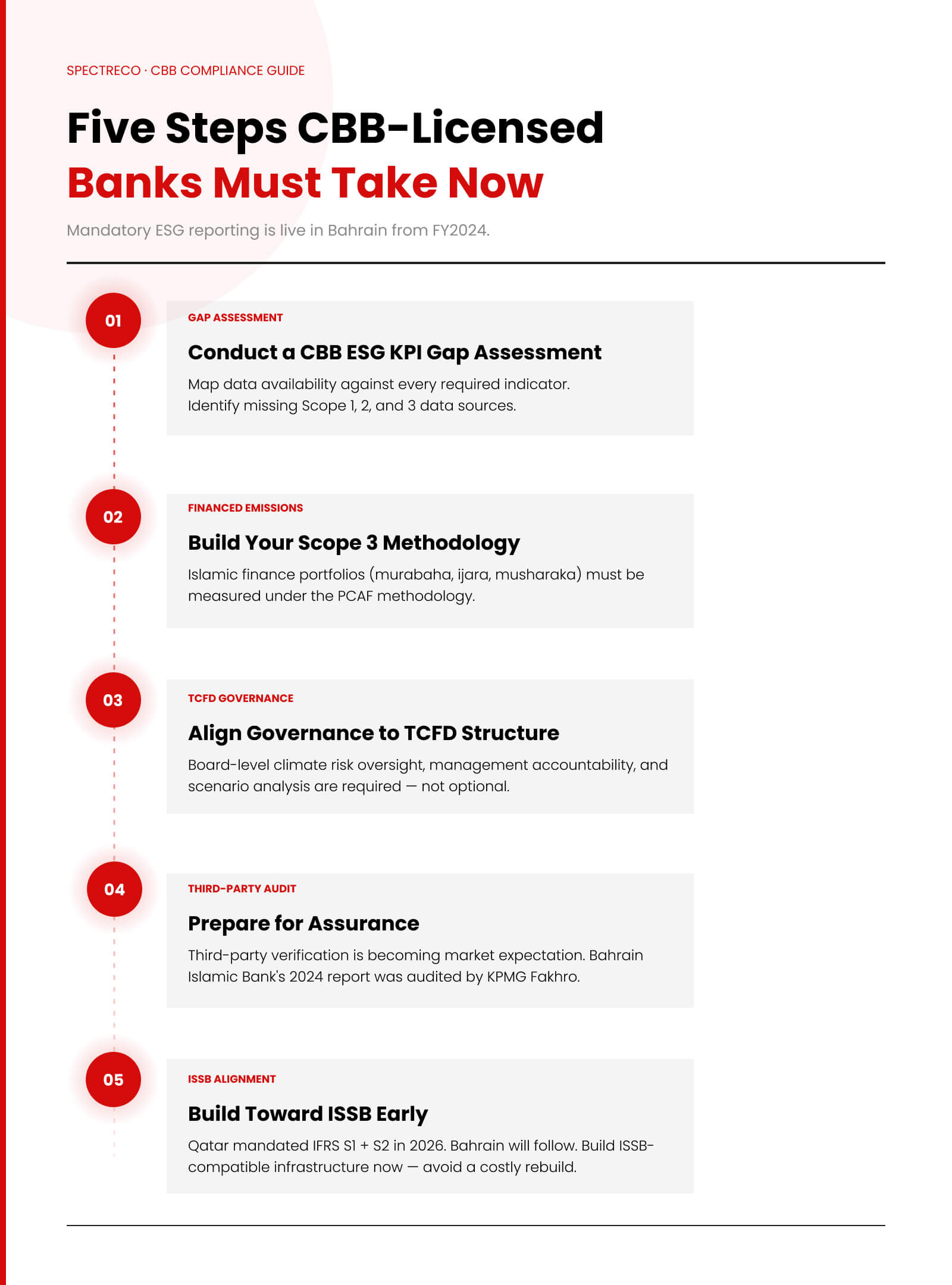

Five Steps CBB-Licensed Banks Must Take Now

- Conduct a gap assessment against the CBB ESG KPI Appendix. Map your current data availability against every required indicator. Identify which Scope 1, 2, and 3 data sources do not yet exist.

- Build your Scope 3 financed emissions methodology. Most banks have not started this. For Bahrain's Islamic banks, financed emissions attached to murabaha, ijara, and musharaka portfolios must be measured under the PCAF (Partnership for Carbon Accounting Financials) methodology. PCAF is the global standard for measuring GHG emissions associated with loans and investments.

- Align governance disclosures to TCFD structure. The CBB module references TCFD. That means board-level documentation of climate risk oversight, management accountability structures, and scenario analysis are required disclosures, not optional additions.

- Prepare for assurance. Bahrain Islamic Bank's 2024 sustainability report was audited by KPMG Fakhro and approved by the Board. Third-party verification is becoming market expectation, not just regulatory direction.

- Build toward ISSB alignment early. The GCC trajectory is clear. Qatar mandated IFRS S1 and S2 in 2026. Saudi Arabia is moving in the same direction. Bahrain will follow. Building ISSB-compatible data infrastructure today avoids an expensive rebuild in 12 to 18 months.

Which Software Solutions Support ESG Reporting Compliance in Bahrain?

The CBB module requires structured data collection across Scope 1, 2, and 3 emissions, plus social and governance KPIs, with annual reporting to a defined KPI structure. Managing that across spreadsheets and disconnected tools compounds errors and creates audit risk. Below are three platforms built for this type of multi-framework, compliance-grade ESG reporting.

1. Spectreco

Spectreco is a sustainability technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore. Its AI-native ESG platform is built for financial institutions operating across multi-jurisdiction regulatory environments, including GCC markets where CBB, QCB, QFCRA, and UAE MOCCAE requirements overlap.

The platform supports portfolio-level ESG analytics, financed emissions measurement under the PCAF (Partnership for Carbon Accounting Financials) methodology, and multi-framework disclosure spanning ISSB, GRI, TCFD, and CBB KPI reporting. For Bahrain's Islamic banks, this matters: measuring financed emissions on murabaha, ijara, and musharaka portfolios requires a PCAF-aligned methodology, not a generic carbon accounting tool.

Spectreco's Compliance, Reporting and Disclosures advisory service pairs the platform with advisory capacity for CBB gap assessments, first-year ESG report preparation, and the transition from initial disclosure to audit-ready, investor-grade reporting. The firm launched the world's first Shariah-compliant ESG Index in partnership with AlBaraka Forum in April 2025, which reflects a level of Islamic finance depth that generic ESG platforms do not carry.

Relevant Spectreco resources for CBB-licensed institutions:

- AI-Native ESG Platform — multi-framework data collection, financed emissions, GCC compliance reporting

- Compliance, Reporting and Disclosures Advisory — CBB gap assessment, audit-ready ESG report preparation

- Virtual Sustainability Office (VSO) — embedded ESG capacity for teams without in-house sustainability expertise

- Climate Finance and Green Capital Advisory — green sukuk structuring and sustainable finance support

2. Persefoni

Persefoni is a carbon accounting and climate disclosure platform purpose-built for financial institutions and large listed corporates. Its Climate Management and Accounting Platform (CMAP) is designed for organisations with material financed emissions exposure, which describes most CBB-licensed banks. The platform covers Scope 1, 2, and 3 emissions measurement under the GHG Protocol, with purpose-built disclosure modules for TCFD, ISSB, CSRD, and CDP.

Persefoni's particular strength for Bahrain banks is its financial sector depth. The platform handles the complexity of measuring Scope 3 Category 15 financed emissions across diversified loan books, an area where general ESG platforms often fall short. Its AI-driven tools, including PersefoniGPT, support anomaly detection and audit-trail documentation to meet the assurance bar that major auditors now apply.

In October 2025, Persefoni formed a strategic partnership with Diligent, a global governance, risk, and compliance (GRC) platform, to integrate carbon accounting with board-level ESG governance workflows. For banks managing TCFD governance disclosures alongside emissions measurement, that combination is relevant.

Source: ESG News, "Diligent and Persefoni Form Strategic Partnership," October 2025; Persefoni.com

3. Sweep

Sweep is an enterprise carbon and ESG management platform founded in France with significant traction across EMEA markets. It was named a Leader in the Verdantix 2026 Green Quadrant for enterprise carbon management, which reflects its positioning among large organisations managing complex, multi-entity ESG data.

The platform centralises ESG and emissions data across organisations and supply chains, with multi-framework reporting capabilities spanning CSRD, GRI, ISSB, TCFD, and CDP. Its workflow-based approach, role-based access controls, and supplier portals are designed for decentralised organisations with multiple business units or cross-border operations. For a Bahraini financial institution with subsidiaries or regional branches across the GCC, Sweep's multi-entity data model is a practical consideration.

Sweep's primary regulatory focus has been European (CSRD and SFDR), which means its GCC-specific regulatory mapping is less developed than Spectreco's. Institutions operating solely within the GCC should confirm the platform's current CBB KPI mapping before committing.

All three platforms require some degree of configuration to produce CBB Appendix 1 KPI-structured outputs. The key differentiator for Bahrain's Islamic banks is financed emissions capability combined with on-the-ground GCC regulatory knowledge. For a structured comparison of what each platform covers, Spectreco's ESG platform page outlines its specific GCC and PCAF capabilities, and the Compliance, Reporting and Disclosures advisory team can run a gap assessment against your current data infrastructure before you commit to a platform.

How Spectreco Supports CBB-Licensed Banks

Spectreco is a sustainability technology and advisory firm with offices in Atlanta, London, Lisbon, and Lahore, working with financial institutions across the GCC on regulatory ESG compliance and sustainable finance structuring. Our financial services ESG platform supports portfolio-level ESG analytics, financed emissions measurement, and multi-framework disclosure across ISSB, GRI, TCFD, and CBB reporting requirements.

Our Compliance, Reporting and Disclosures advisory service is designed for CFOs and compliance officers who need to move from first-year ESG reports to audit-ready, investor-grade disclosures across multiple GCC jurisdictions.

We launched the world's first Shariah-compliant ESG Index in partnership with AlBaraka Forum in April 2025. Our GCC advisory team understands both the regulatory requirements and the Islamic finance structures that shape Bahrain's banking sector.

For CBB-licensed banks that have not yet started their ESG reporting programme, or that need to upgrade from a first-attempt disclosure to a compliant and credible framework, Spectreco offers a 30-minute compliance gap assessment. Contact our GCC team to start.

Frequently Asked Questions

More From Our Blog

Your ESG Journey?